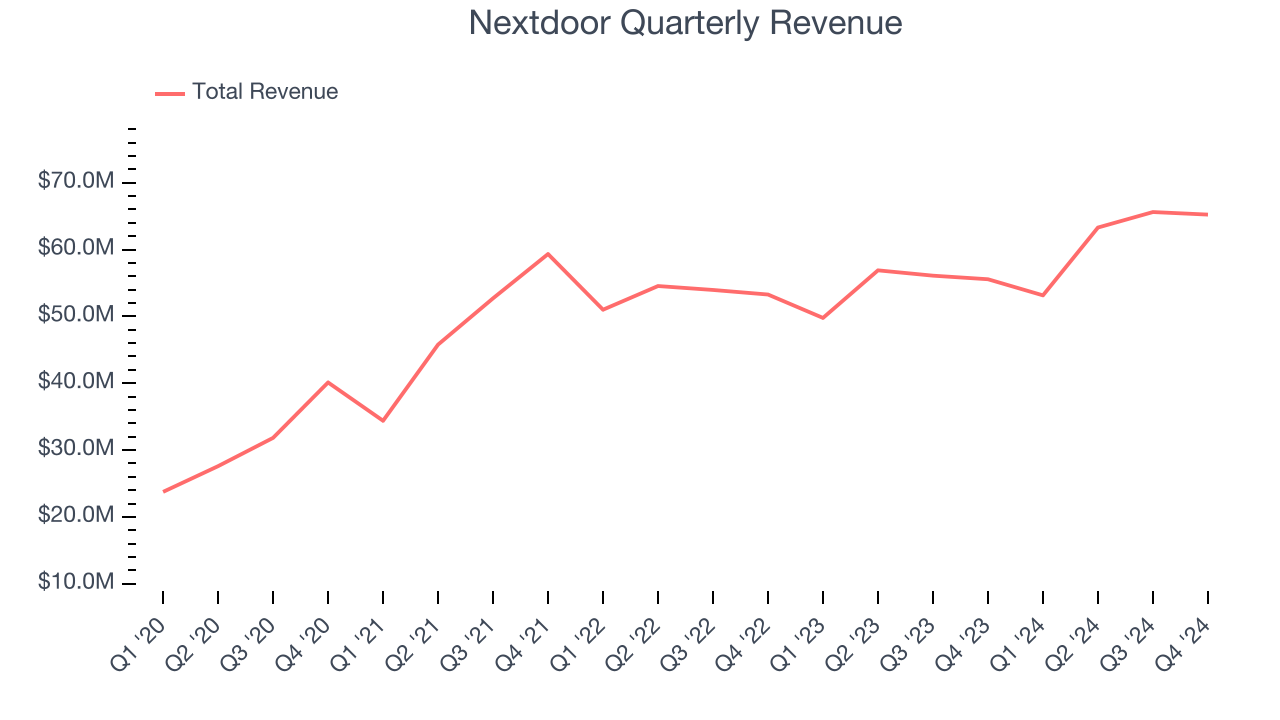

Neighborhood social network Nextdoor (NYSE:KIND) beat Wall Street’s revenue expectations in Q4 CY2024, with sales up 17.4% year on year to $65.23 million. On the other hand, next quarter’s revenue guidance of $53 million was less impressive, coming in 13.7% below analysts’ estimates. Its GAAP loss of $0.03 per share was $0.01 above analysts’ consensus estimates.

Is now the time to buy Nextdoor? Find out by accessing our full research report, it’s free.

Nextdoor (KIND) Q4 CY2024 Highlights:

- Revenue: $65.23 million vs analyst estimates of $64.18 million (17.4% year-on-year growth, 1.6% beat)

- EPS (GAAP): -$0.03 vs analyst estimates of -$0.04 ($0.01 beat)

- Adjusted EBITDA: $3.04 million vs analyst estimates of -$2.07 million (4.7% margin, significant beat)

- Revenue Guidance for Q1 CY2025 is $53 million at the midpoint, below analyst estimates of $61.43 million

- EBITDA guidance for Q1 CY2025 is -$13 million at the midpoint, below analyst estimates of -$9.91 million

- Operating Margin: -26.2%, up from -85.8% in the same quarter last year

- Free Cash Flow was $11.67 million, up from -$13.17 million in the previous quarter

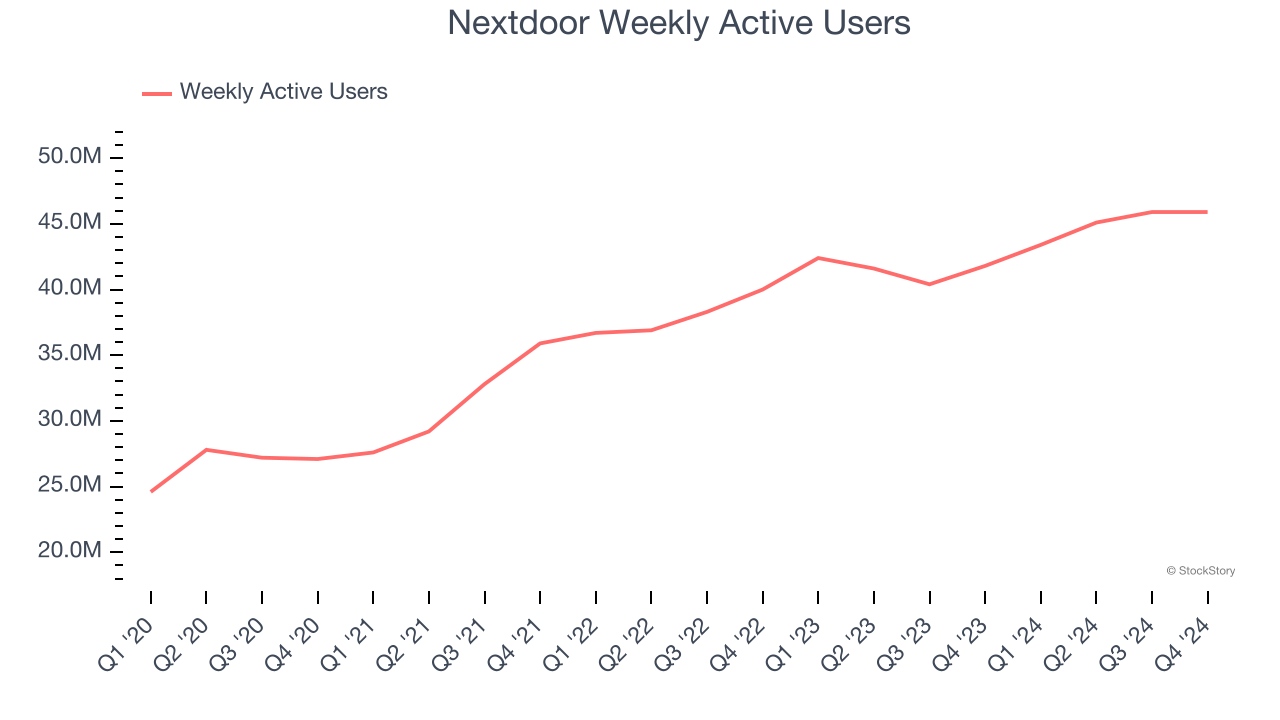

- Weekly Active Users: 45.9 million, up 4.1 million year on year

- Market Capitalization: $974.5 million

Company Overview

Helping residents figure out what’s happening on their block in real time, Nextdoor (NYSE:KIND) is a social network that connects neighbors with each other and with local businesses.

Social Networking

Businesses must meet their customers where they are, which over the past decade has come to mean on social networks. In 2020, users spent over 2.5 hours a day on social networks, a figure that has increased every year since measurement began. As a result, businesses continue to shift their advertising and marketing dollars online.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last three years, Nextdoor grew its sales at a mediocre 8.8% compounded annual growth rate. This was below our standard for the consumer internet sector and is a tough starting point for our analysis.

This quarter, Nextdoor reported year-on-year revenue growth of 17.4%, and its $65.23 million of revenue exceeded Wall Street’s estimates by 1.6%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.9% over the next 12 months, an acceleration versus the last three years. This projection is admirable and implies its newer products and services will spur better top-line performance.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Weekly Active Users

User Growth

As a social network, Nextdoor generates revenue growth by increasing its user base and charging advertisers more for the ads each user is shown.

Over the last two years, Nextdoor’s weekly active users, a key performance metric for the company, increased by 9.1% annually to 45.9 million in the latest quarter. This growth rate is solid for a consumer internet business and indicates people are excited about its offerings.

In Q4, Nextdoor added 4.1 million weekly active users, leading to 9.8% year-on-year growth. The quarterly print isn’t too different from its two-year result, suggesting its new initiatives aren’t accelerating user growth just yet.

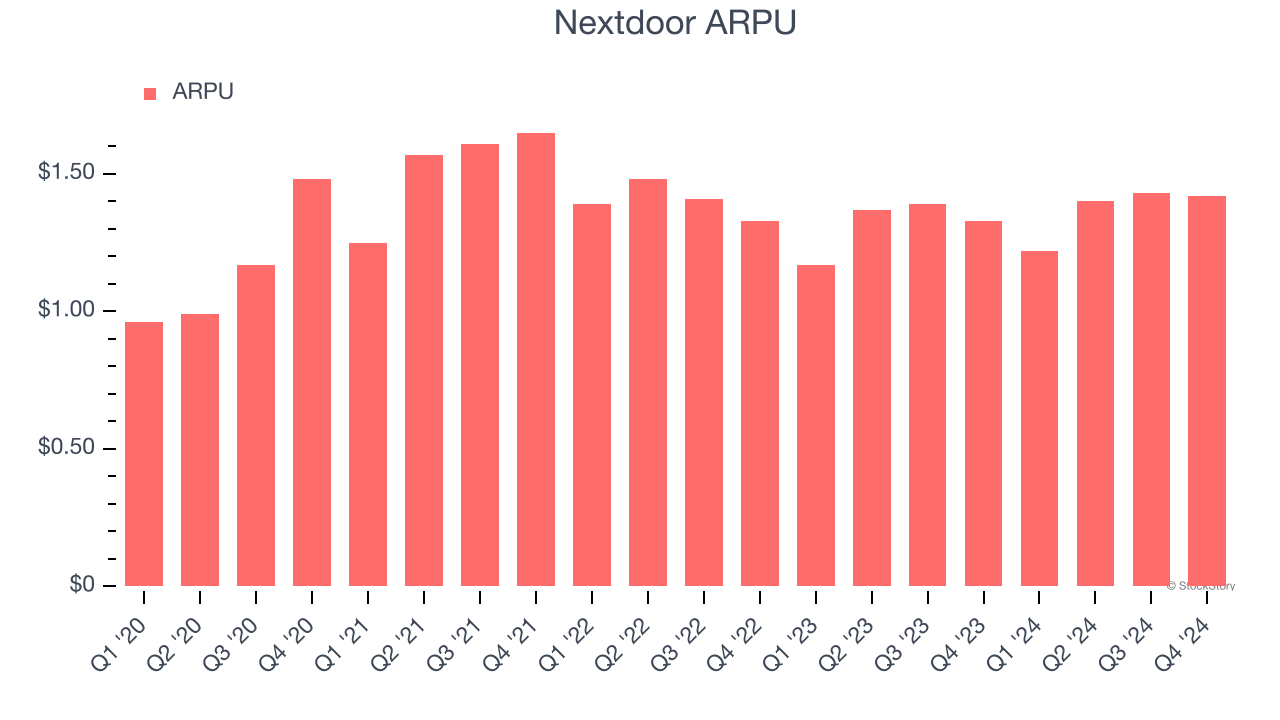

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track for social networking businesses like Nextdoor because it measures how much the company earns from the ads shown to its users. ARPU can also be a proxy for how valuable advertisers find Nextdoor’s audience and its ad-targeting capabilities.

Nextdoor’s ARPU fell over the last two years, averaging 1.1% annual declines. This isn’t great, but the increase in weekly active users is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Nextdoor tries boosting ARPU by taking a more aggressive approach to monetization, it’s unclear whether users can continue growing at the current pace.

This quarter, Nextdoor’s ARPU clocked in at $1.42. It grew by 6.8% year on year, slower than its user growth.

Key Takeaways from Nextdoor’s Q4 Results

We were impressed by how significantly Nextdoor blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue and EPS outperformed Wall Street’s estimates. On the other hand, its number of weekly active users missed while its revenue and EBITDA guidance for next quarter fell short, making this a softer print. The stock traded down 11.2% to $2.21 immediately after reporting.

Nextdoor didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.